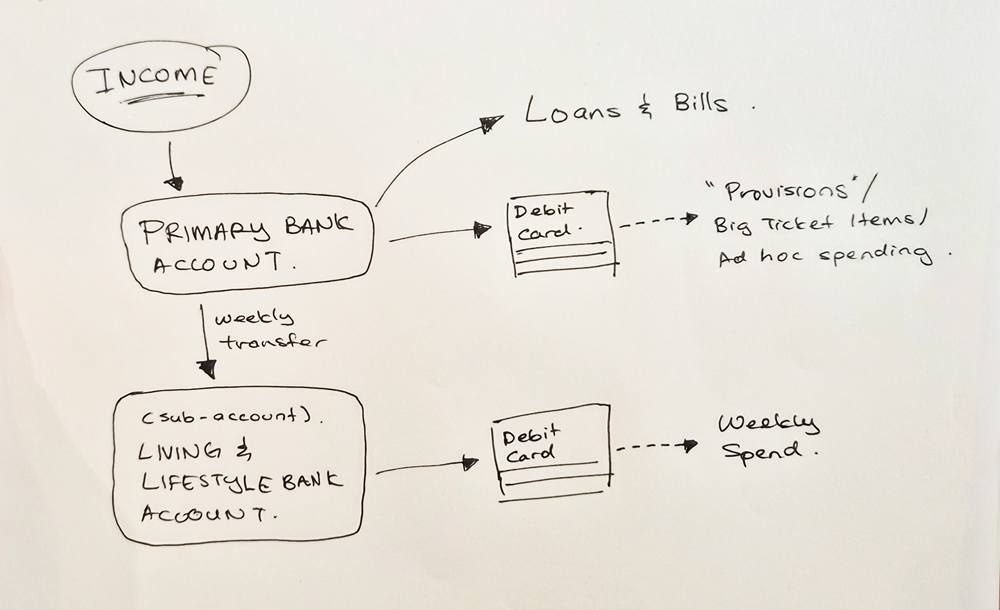

All your income (PAYG, investments etc)

should go into one primary bank account.

If you have a mortgage, this will be a 100% offset account.

If you don't, it'll be a high interest savings account.

Make sure your weekly allowance is transferring

each week into your Living & Lifestyle account

– so you have your 7-day float up and running.

Create a separate sub-Bank Account for weekly allowances.

Your loans repayment and bills payment

should be set up as direct payments.

Do not bring this debit card out.

Keep it at home and only use it

when you plan to spend on those

Provision expenses.

Use the debit card for all of your provision spending.

Make sure to take note how much you've spent so

you can keep track of how much provision you've left!

(Moorr Mobile app can simplify this 😉)

IMPORTANT: This must be a debit card.

The highest money leakage is usually in our

regular spending so this needs to be a

debit card to stop that leakage.

If you run out of funds in this account,

you know that you are overspending!

Hence stopping that unconscious spending!

Try and identify non-essential expense items

in this category. By cutting back on these, you

could save extra per week, which could be

used towards your goal.

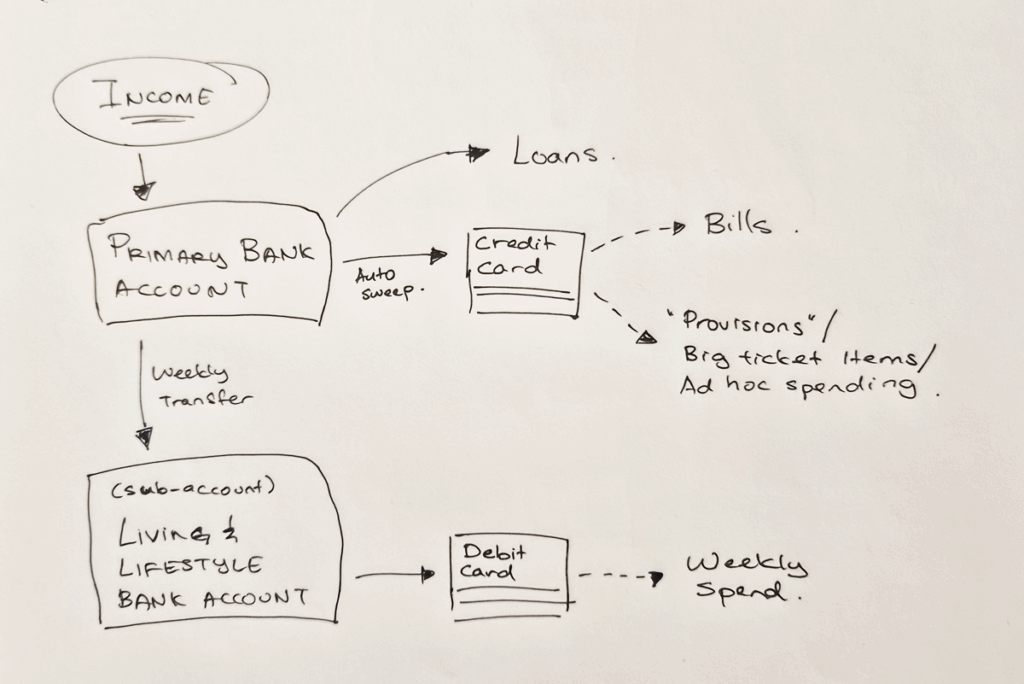

All your income (PAYG, investments etc)

should go into one primary bank account.

If you have a mortgage, this will be a 100% offset account.

If you don't, it'll be a high interest savings account.

Make sure your weekly allowance is transferring

each week into your Living & Lifestyle account

– so you have your 7-day float up and running.

Create a separate sub-Bank Account for weekly allowances.

Your loans repayment should be

set up as direct payments.

Set up an autosweep for your credit card payment.

Any outstanding balance on your credit card

should be paid off automatically so you don't

incur any credit card interest.

Interest is calculated daily so we want

to make sure your money stays in the

offset account for as long as possible,

hence, saving you those daily interest payment.

Keep your bill spending down and shop for better deals!

Make sure to take note how much you've spent so

you can keep track of how much provision you've left!

(Moorr Mobile app can simplify this 😉)

IMPORTANT: This must be a debit card.

The highest money leakage is usually in our

regular spending so this needs to be a

debit card to stop that leakage.

If you run out of funds in this account,

you know that you are overspending!

Hence stopping that unconscious spending!

Try and identify non-essential expense items

in this category. By cutting back on these, you

could save extra per week, which could be

used towards your goal.

So much to realise & gain,

nothing to lose.

Onboard with your hopes,

dreams & finances.

Start planning & living your

Lifestyle-by-Design.

So much to realise & gain,

nothing to lose.

Onboard with your hopes,

dreams & finances.

Start planning & living your

Lifestyle-by-Design.

So much to realise & gain,

nothing to lose.

Onboard with your hopes,

dreams & finances.

Start planning & living your

Lifestyle-by-Design.

So much to realise & gain,

nothing to lose.

Onboard with your hopes,

dreams & finances.

Start planning & living your

Lifestyle-by-Design.