Your Yearly Remaining Provisions Total is effectively a representation of your ‘Provisions Jar’ broken down on a rolling monthly basis. Your ‘Monthly Allocated Provisions Spending’ is the amount you allocate to your Provisions Jar each month. For example, an amount of $500 per month is your Monthly Allocated Provision Spending, based on an annual provision allocation of $6,000. As the months progress, you add funds into this Jar based on your monthly allocation, and as you spend money, you reduce the balance in your Provisions Jar.

Expanding on this example, if your actual Provisions Spent during your first month was $300, your Yearly Remaining Provisions Total would increase by $200, indicating that you underspent during that month($500 minus $300). This $200 left over in your Provisions Jar would then carry forward to the next month and be added to your new month’s $500 allocation ($500 plus $200 = $700).

If you spend $600 in the second month—exceeding your usual $500 monthly allocation—your Yearly Remaining Provisions Total would be calculated as $700 (carried-forward Yearly Remaining Provisions Total) minus $600, leaving you with a $100 in your Provisions Jar.

During months when you have higher expenses due to large-ticket items, such as a major holiday airfare, your Yearly Remaining Provisions Total might temporarily dip into negative territory. However, and most importantly, as long as you adhere to your overall Provisions Jar allocation, your Yearly Remaining Provisions Total should gradually recover, provided you don’t overspend.

It’s perfectly fine if your Yearly Remaining Provisions Total hovers around the $0 mark, as this indicates you’re on track with your planned provision spending. However, keeping this total positive should be your goal, as any unspent provisions at the end of the year can result in an additional surplus cash position providing additional financial savings & flexibility.

[insert diagram/illustration of table + graph overlay to show the example of the above]

The Remaining Provision Balance displayed under the Provisions Jar component reflects the amount remaining on an annual basis, whereas your Yearly Remaining Provisions Total represents the allocation to your Provisions Jar on a rolling monthly basis.

For example, some MoneySMARTS users might have large provisions allocated—say $30,000 per year—across all their expense cards they have allocated under the Provisions Jars. However, your actual cash in the bank might only be $20,000 at the start of the MoneySMARTS 12-month period (understanding that new money earnt will also be coming in each month). The MoneySMARTS system understand this and is designed to accommodate this by provisions money on a monthly basis, even though this allocation is based on an annual calculation.

This approach helps you better track your cashflow by incorporating your anticipated Provisions as monthly values into your monthly target surplus calculations.

[illustrative example]

Previously, in MoneySMARTS 1.0, the Yearly Remaining Provisions Chart reflected the latest annualized value of your Provisions Jar balance, calculated as the starting allocation minus the amount spent during the period. However, under this version, changes to your financial circumstances weren’t captured historically, which affected your overall calculations for the entire period. The problem with that approach was that any adjustments made later in the period were retroactively applied, making it seem as though the changes were in place from the start, meaning it was hard to really see the progress you are making towards your targeted monthly surplus.

For example, if a user initially set a $5,000 annual provision spend, but during the 12-month period, they increased their annual Provisions Jar allocation to $15,000pa in month 10, MoneySMARTS 1.0 would incorrectly treat this $15,000 as if it had been allocated from month 1. This approach distorted the Yearly Remaining Provisions Chart by overestimating the available funds.

In contrast, the new MoneySMARTS 2.0 Yearly Remaining Provisions chart, is now consistent with the chart outlined in the Money Made Simple Again book, which tracks changes on a rolling monthly basis. This means that if you increase your Provisions Jar allocation to $15,000pa in month 10, it adjusts your Monthly Allocated Provisions Spending by an additional $833.33 per month (an increase of $10,000 spread over the remaining 12 months) from month 10 onwards, rather than allocating an additional $5,000 for each of the remaining two months. This approach avoids distorting your targeted monthly surplus.

Note: If this $10,000 was a figure you initially missed in setting up your 12-month MoneySMARTS targets, and you wanted to include this $10,000 to apply from the start of the period, the good news is that you can now update your historical records in your MyFINANCIAL Expense Card or cards. This allows you to set the correct starting value for your Provisions Jar, ensuring that the entire MoneySMARTS period accurately reflects your financial plan.

Furthermore, with the upgrade to MoneySMARTS 2.0, whenever there is a significant new financial change to your numbers, we’d recommend you perform a MoneySMARTS Rollover to reset your next 12-months range, even if you haven’t completed a full 12 month period.

In MoneySMARTS 1.0, if you’d archived a provision or changed a jar within a period, it wouldn’t be shown at all and you’d lose track of the spending that occured within this provision, as well as the original amount allocated to this expense.

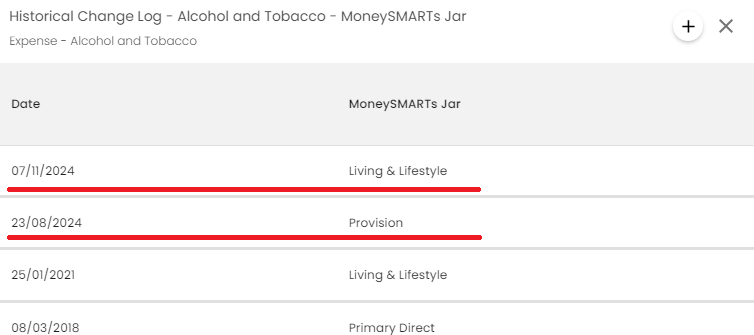

In MoneySMARTS 2.0, this is displayed in a separate area underneath the standard provision jar widget. This shows any provision expenses that were either archived or changed from a provision jar to a different jar within the displayed period, shown as ‘Active from’ the start date of the period to the date the expense ceased to be a provision, or was archived.

This has been included to help you reconcile your figures, as changes to your historical figures are now always included in MoneySMARTS and will reflect as such in the check up reporting table.

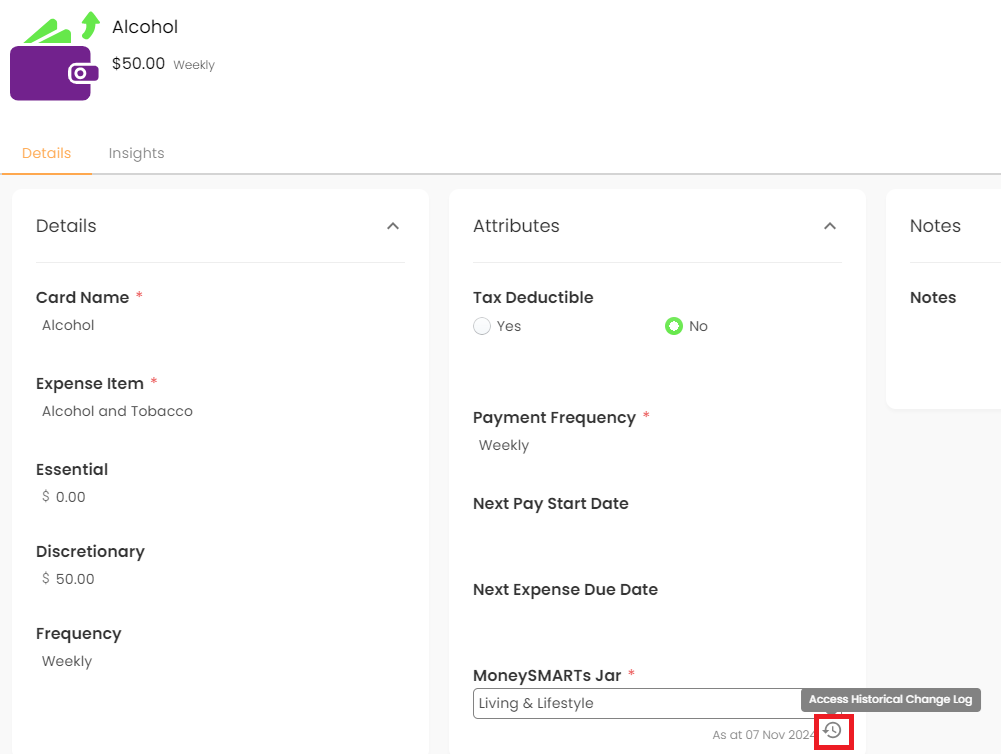

Data in MoneySMARTS 2.0 is displayed based on the Historical Data contained within your MyFINANCIAL Cards. This includes allocations to your Jars, which are also historically tracked.

If the most recent changes have not displayed on your MoneySMARTS page, please follow the below steps before contacting our support:

Yes, absolutely! All these new updates are on both mobile and web.

There’s only one exception and that’s the annual rollover feature. The annual rollover requires a little bit more input from the users so unfortunately, there’s simply not enough space on a mobile screen to support this. Hence, for the best user experience, the rollover is only available on the web version.

Good news is none of your existing data is affected or lost.

For any historically entered check-ups, your information will be retained as singular account balance records. You’ll be able to still view and edit these, though for past records, you’ll also be able to choose to use the check-up process.

The checkups display the balances of the bank accounts or credit cards as at the specified check up date.

This means that balances between two checkup dates will not be shown.

MoneySMARTS 1.0 was developed in 2017 and initially worked on displaying only the latest figures on the MoneySMARTS page.

Let’s say for example you had a start date of 1st January 2023 with a MoneySMARTS period between 1st January 2023 – 31st December 2023. If you’d made changes to your loan repayments or income in November 2023, you’d see these changes reflected all the way back to January 2023, resulting in an incorrect display of your MoneySMARTS position as of January 2023 all the way through to November 2023.

MoneySMARTS 2.0 works to correct this, and now utilises historical tracking (like the rest of the insights in Moorr) to much more accurately record and reflect your financial position at any point during the MoneySMARTS period.

Because of this, you’ll more than likely see differences to your figures, both in past and current MoneySMARTS Periods.

The primary reason for this is normally that the historical entries for your income, expense or borrowings items likely did not occur until later in the period. To fix this, double check your historical entries under the cards, notably the as at dates for the values, ownership and jar, and add the correct entries to the right historical dates.

The Accumulated Actual Surplus is based on the calculation: Current Month’s Ending Net Cash Position – Current Month’s Yearly Remaining Provisions Total – Starting Net Cash Position. This specific calculation recognises that provisions for the month are not necessarily all spent, and in some months more than the allocated monthly provision is spent.

Now let’s say for example you had an unforecasted expense of an additional $10,000 in July 2024 on your holiday provision. If you’d paid in cash, you’d expect to see a direct decrease in your Account Balance by the $10,000 during that month, or if purchased on credit, for the Credit Card balance to increase by $10,000 for that month.

If your Ending Cash balance still increased even though you were expecting the total net position to decrease during the month, this additional balance increase is recognised as additional surplus.

Because you have still managed to increase your account balance for that month and the months thereafter, the accumulated actual surplus reflects this position – that you have managed to overspend on your yearly provisions yet still managed to increase your overall net cash position over time.

MoneySMARTS 2.0 leverages the historical data within MyFINANCIALS, paving the way for bank connectivity in the future. This enhancement ensures that all check-up balances are automatically updated and recorded in your MyFINANCIAL Cards’ historical change logs whenever you perform an update.

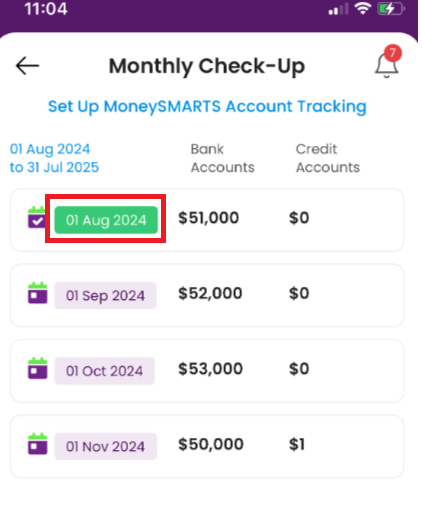

However, it’s important to note that future-dated check-ups will not appear until the specified date arrives.

For example, if today is 20 November 2024 and your next check-up is scheduled for 1 December 2024, the December check-up will only become visible on 1 December. This approach ensures that the balances accurately reflect the actual bank data as of the check-up date.

Recording balances prematurely could result in overstating or understating the actual figures for 1 December, potentially leading to an inaccurate representation of your financial data.

Don’t worry! Your provision data hasn’t disappeared.

This is likely because your Start Date has not been set correctly, which is common amongst users who only use the page for tracking their Provision Transactions but hadn’t utilised the full fledged check-up functionality in the past. Because the Start Date was not correctly set, the page is simply displaying data for an older period. In these cases, you’ll get the below error message:

To change your start date, it’s easy. If you’re on the Web, simply click the ‘Start Date’ field and change it to a new date. If you’re on the Mobile App, simply click the Green Date, like below, to change the Start Date.

You can also follow the steps in this Youtube video.

If you’re keen to adopt MoneySMARTS but not sure where to start, then check out our step by step guide here >